The Invariants of AI: What Remains Defensible When Intelligence Commoditizes

A Strategic Research Report for Investors and Thought Leaders

Abstract

This report investigates the invariant properties of AI — the durable, structural characteristics of AI systems and their deployment that determine which businesses win over the long term. The central thesis is that the invariants of AI are not found in model performance, which is converging rapidly across competitors, but in the physical constraints that surround intelligence and the self-reinforcing systems that companies build to harness it.

Drawing on foundational economic theory, systems thinking, and a competitive landscape analysis of major AI players, we lay out three categories of invariants. Two are structural: the physical supply chain and energy infrastructure. The third, and the focus of this exploration, is generative: a self-reinforcing flywheel composed of proprietary data, human orchestration, agentic context, post-training know-how, and workflow embeddedness.

The implications to builders, founders and companies at large is that the elusive “moats” in the era of AI exist, but rather than being a static structure to be acquired or implemented, it is a system of human capabilities, data and feedback loops.

Because the AI space ahead of us seems utterly unpredictable, this study began with a simple question, “what are the things that will not change in the next 5 years?”, rather than “what are the things that will change”? Here’s we arrived:

1. The Structural Invariants: The Terrain of Scarcity

The first two invariants we found are structural. They exist independent of any company's software strategy. They are features of the physical and institutional environment — permanent constraints that capital alone cannot eliminate on any reasonable timeline.

Invariant A: Physical Supply Chain Chokepoints

The most durable moats in the AI era are not digital — they are physical. The entire AI compute stack is dependent on a hyper-concentrated, geopolitically sensitive supply chain that took decades to construct.

The Lithography Monopoly. ASML, a Dutch company headquartered in Veldhoven, holds an effective 100% monopoly on the Extreme Ultraviolet (EUV) lithography machines required to manufacture advanced AI chips [7]. The engineering required to produce EUV light represents 30 years of accumulated investment and supplier relationships that cannot be recreated.

The Manufacturing Chokepoint. TSMC controls approximately 71% of the global contract chip manufacturing market [9]. The gap between TSMC and its competitors is not simply a matter of installed capacity; it reflects decades of process technology advancement, yield optimization, and operational expertise. Every major AI accelerator — NVIDIA's H100 and Blackwell families, Google's TPUs, Apple's custom silicon — is manufactured at TSMC.

These chokepoints act as tollbooths. ASML and TSMC capture value regardless of which software or model company wins the competitive race at higher layers of the stack.

Invariant B: Energy Infrastructure

Energy is the constraint beneath the constraint. ASML machines and TSMC fabs are useless without the power to run the data centers they supply. As AI data centers proliferate, the primary constraint on AI growth has shifted from capital to grid connectivity and generation capacity.

Some forecasts suggest that AI alone could drive a 165% increase in power demand by 2030 [10]. As of mid-2026, over 700 data centers were under construction globally, and grid connectivity had emerged as the single most cited commercial risk for AI data center expansion [11].

Energy has all the hallmarks of a genuine structural invariant:

- It is physical and finite; permitting, construction, and interconnection queues mean new power infrastructure takes 5–15 years to bring online.

- It is geographically concentrated; access to cheap, reliable, low-carbon power is not uniformly distributed.

Hyperscalers including Microsoft, Google, and Amazon have recognized this invariant, entering into 20-year Power Purchase Agreements (PPAs) for nuclear energy and investing in Small Modular Reactor (SMR) development [12]. The companies that secure long-term generation capacity and grid interconnection rights possess a structural advantage that latecomers simply cannot replicate at equivalent cost.

3. Invariant C: The Generative Flywheel

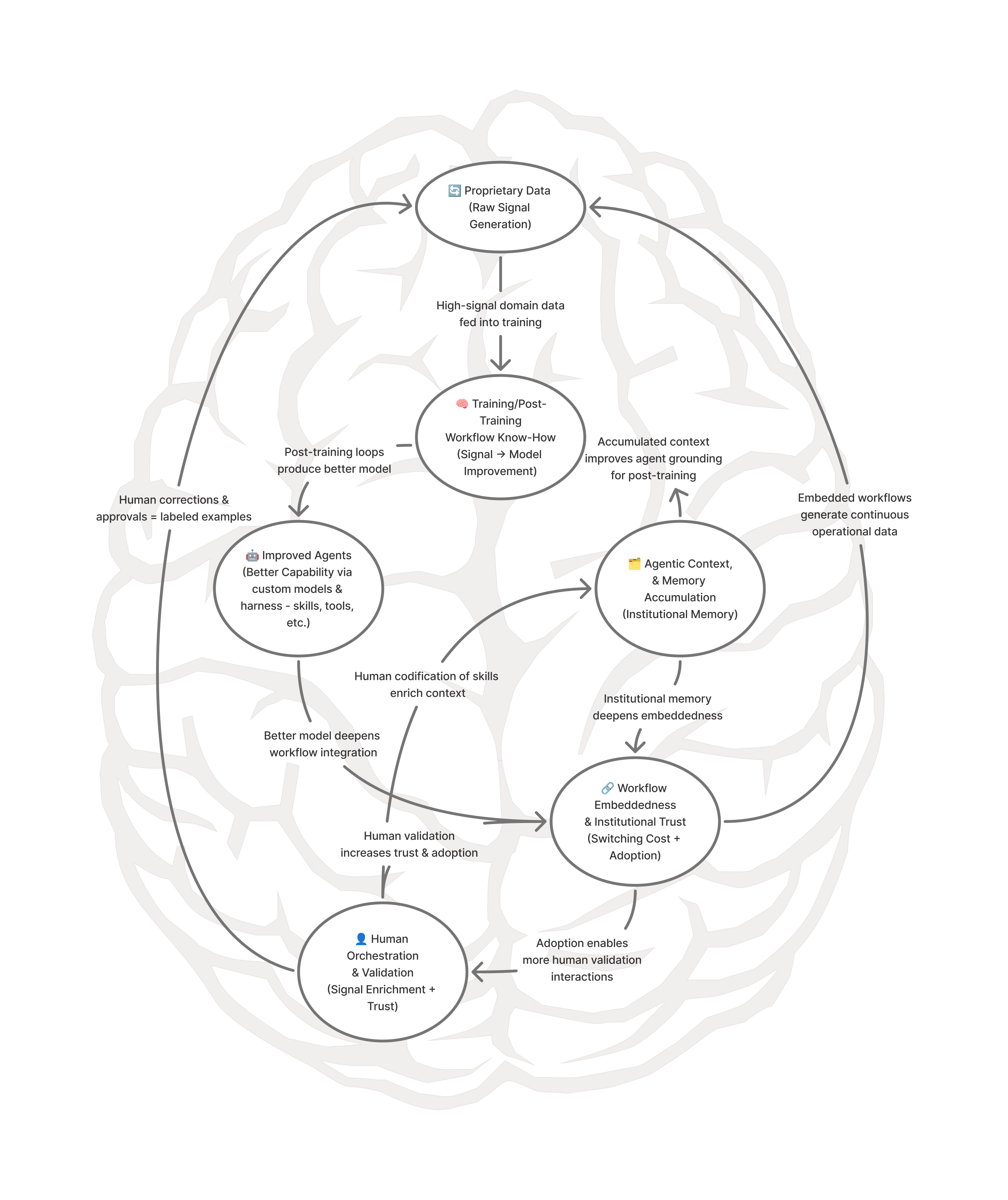

If the structural invariants are the terrain, the generative invariant is the engine that companies build to traverse it. The generative invariant is not a single moat, but a self-reinforcing system — a flywheel composed of five interlocking components. These components do not operate independently; they are causally linked. A company that owns all five has a compounding advantage that accelerates over time. A company missing any component has a structural vulnerability.

Component 1: The Proprietary Data Flywheel

The a16z essay "The Empty Promise of Data Moats" (2019) warned against naive data accumulation strategies. It argued that static data is not a moat because the marginal value of incremental data decreases, the cost of acquiring it increases, and competitors can often bootstrap equivalent datasets [13].

What is a genuine moat is the closed-loop flywheel — systems that continuously generate high-signal, proprietary training data as a byproduct of commercial operations. The distinction matters enormously. Tesla's autonomous driving data moat is real because every mile driven by a consumer vehicle generates edge-case data that simulation cannot produce [14].

Component 2: Human Orchestration and Validation

“Human-in-the-loop” is not a temporary inefficiency to be engineered away. In high-stakes domains, for instance, AI outputs require human accountability by legal and institutional mandate. This is not a transitional arrangement pending better AI; regulatory pressure is intensifying rather than relaxing as AI becomes more capable [17].

Human orchestration performs two functions simultaneously. First, it is the trust mechanism that makes AI deployable: validated outputs build institutional confidence. Second, it is the primary source of the proprietary training signal for Component 1. Every human correction is a labeled training example generated by a domain expert in real operational conditions — a quality of signal that crowd-sourced annotation cannot match.

This component is also the flywheel's anti-fragility mechanism. When failures occur, the human validation layer catches the error before it erodes trust, and converts it into the highest-signal training data possible. The system gets stronger from being stressed. Without this layer, failures cut off the training signal and cause the flywheel to decelerate. Palantir AIP, Harvey, and Abridge all exemplify this architecture.

Component 3: Agentic Context and Memory Accumulation

As AI moves from chatbots to autonomous agents, the relevant unit of competitive advantage shifts from data to context — the dynamic, multi-layered operational reality of a specific business.

Context encompasses data when built correctly: it includes behavioral patterns, relationship histories, temporal understanding, and situational awareness [15]. Companies that build sophisticated memory architectures are building moats that compound over time as agents accumulate institutional knowledge specific to their operational environment.

Component 4: Post-Training Workflow Know-How

The organizational capability to run sophisticated post-training processes is the mechanism that converts proprietary data and human feedback into continuously improving models.

This capability (encompassing RLHF (Reinforcement Learning from Human Feedback), DPO (Direct Preference Optimization), evaluation infrastructure, etc.) must be earned. The gap between reading a research paper and running a post-training pipeline at scale is enormous. It requires years of accumulated engineering judgment and institutional memory.

The leading edge of this capability is autonomous self-improvement. Andrej Karpathy's concept of autoresearch — an autonomous agent loop that runs hundreds of experiments overnight, keeps improvements, and discards failures — points to a future where AI systems conduct their own R&D using proprietary context [16]. When applied to proprietary domain data, this becomes a self-improving system that compounds at the speed of compute, not the speed of human researchers.

Component 5: Workflow Embeddedness and Institutional Trust

The final component of the flywheel describes how a model becomes adopted and indispensable. In enterprise and regulated industries, the best model does not win; the most trusted and deeply integrated system wins.

Embeddedness occurs in three layers [17]:

- Technical integration: AI capabilities integrated directly into core systems (CRM, ERP), making workflow migration expensive.

- Learning integration: Systems that learn from proprietary data through feedback loops, becoming increasingly valuable over time.

- Human integration: Employees who become comfortable with and reliant on the solution, creating organizational resistance to change.

In regulated industries, trust itself is a structural moat. Companies that solve the "last mile" of reliability, auditability, and compliance — such as Palantir's data ontology in defense, or Harvey's legal AI — build moats based on institutional trust that raw intelligence cannot overcome [18].

4. Competitive Landscape Analysis

How are the major technology players positioned against these invariants?

| Company | Structural Invariants (A & B) | Generative Flywheel (C) | Strategic Position |

|---|---|---|---|

| ASML / TSMC | Absolute Monopoly | N/A | The physical tollbooths of the AI era. |

| NVIDIA | High (Silicon design) | High (CUDA ecosystem lock-in) | Dominant, but faces long-term threat from custom inference ASICs. |

| High (Custom TPUs, Energy) | Very High (Full-stack flywheel) | Architecturally coherent, combining custom silicon, frontier models, and massive distribution data flywheels. | |

| Microsoft | High (Energy PPAs) | High (Distribution & Embeddedness) | Leverages unparalleled enterprise distribution, but vulnerable due to OpenAI model dependency. |

| OpenAI | Low (Dependent on MSFT) | Medium (Brand & Consumer scale) | Weakest structural moat; heavily reliant on hyper-growth and brand recognition before model commoditization completes. |

| Anthropic | Low (Dependent on AWS/GCP) | High (Trust & Post-Training) | Deliberate focus on safety and enterprise trust creates a distinct brand moat in regulated industries. |

| Meta | Low | High (Distribution & Open Source) | "Commoditize your complement" strategy protects its core advertising distribution moat while forcing competitors to spend against a free product. |

| Palantir | Low | Very High (Trust & Orchestration) | The premier example of workflow embeddedness and institutional trust via its proprietary data ontology. |

| Tesla | Medium (Dojo supercomputer) | Very High (Physical Data Flywheel) | Real-world edge-case data generates a compounding advantage that simulation cannot match. |

| Vertical SaaS (e.g., Harvey, Abridge) | Low | High (Domain Context & Orchestration) | Success relies on acquiring proprietary industry data and embedding directly into specialized human-in-the-loop workflows. |

5. Conclusion: Strategy for the Agentic Era

As the AI industry matures from the "chatbot era" to the "agentic era," the illusion that raw model capability is a sustainable business model is fading. Intelligence is becoming a utility — abundant, cheap, and universally accessible.

For investors and operators, the strategic mandate is clear: Do not invest in intelligence; invest in the constraints around intelligence.

Value will accrue to those who control the physical chokepoints (silicon, energy), those who build self-reinforcing data flywheels, those who orchestrate human validation to create anti-fragile systems, those who master post-training improvement loops, and those who embed their context so deeply into enterprise workflows that they become indispensable.

Business durability is not a feature you can build directly; it is an emergent property of a system running these loops successfully over time. In the age of infinite AI, the invariants of business — physical reality, proprietary context, and institutional trust — remain as vital as ever.

References

[1] TechPolicy.Press. (2025). Taking AI Commoditization Seriously.

[2] VKTR. (2025). Moats or Myths? How OpenAI, Anthropic and Google Plan to Stay on Top.

[3] Evans, B. (2026). How will OpenAI compete?

[4] Sutton, R. (2019). The Bitter Lesson.

[5] Christensen, C., & Raynor, M. (2003). The Innovator's Solution: Creating and Sustaining Successful Growth.

[6] NPR Planet Money. (2025). Why the AI world is suddenly obsessed with Jevons paradox.

[7] The Generalist. (2023). ASML: A Monopoly on Magic.

[8] Baker, A. (2026). Why Is NVIDIA the Most Valuable Company in the World? The AI Stack, the CUDA Moat, and the Threats That Could Unseat It.

[9] TSMC. (2025). TSMC Intends to Expand Its Investment in the United States.

[10] America's for Prosperity. (2025). America's Energy Bottleneck: The Hidden Constraint on AI, Industry, and National Competitiveness.

[11] EnkiAI. (2026). AI Data Center Grid Strain: Power Halts Growth in 2026.

[12] Introl. (2026). Nuclear power for AI: inside the data center energy deals.

[13] Andreessen Horowitz. (2019). The Empty Promise of Data Moats.

[14] Road to Autonomy. (2026). Tesla's Data Advantage.

[15] Decoding Discontinuity. (2025). Second Law of Value in the Agentic Era: Context is the New Moat.

[16] Fortune. (2026). 'The Karpathy Loop': 700 experiments, 2 days, and a glimpse of autonomous AI agents future.

[17] McKinsey & Company. (2026). From AI table stakes to AI advantage: Building competitive moats.

[18] Pangeanic. (2026). Why Palantir's ontologies are its deepest (and dangerous) moat.

[19] Tung, T. & Roussiere, P. (2026). Tacit Knowledge Is Your Next Competitive Moat. California Management Review.